(Part 1 in a blog series focusing on prepaid tuition plans)

By Betty Lochner

Director, Guaranteed Education Tuition October 5, 2012

As director of Washington’s Prepaid Tuition Plan, I often hear parents say, “We decided to put our money in a 529 College Savings Plan instead of GET.” To which I always reply, “GET is a 529 college savings plan.”

There is a lot of information out there that can lead people to think that a Prepaid Tuition plan (or Prepaid plan) is different from 529 College Savings Plans (or Savings Plan). Well, they are and they aren’t. This blog series should help shed some light on those differences.

First, of all, here are some Fun Prepaid Facts

Prepaid Tuition Plans were the first state-administered college savings plans to be offered by several states in the late 1980’s. College Savings Plans became popular when Congress passed legislation in 1996 creating Section 529 of the Internal Revenue Code.

There are currently more than 1.3 million prepaid accounts nationwide, valued at nearly $22 billion. Tuition plans have helped hundreds of thousands of students pay for college tuition.

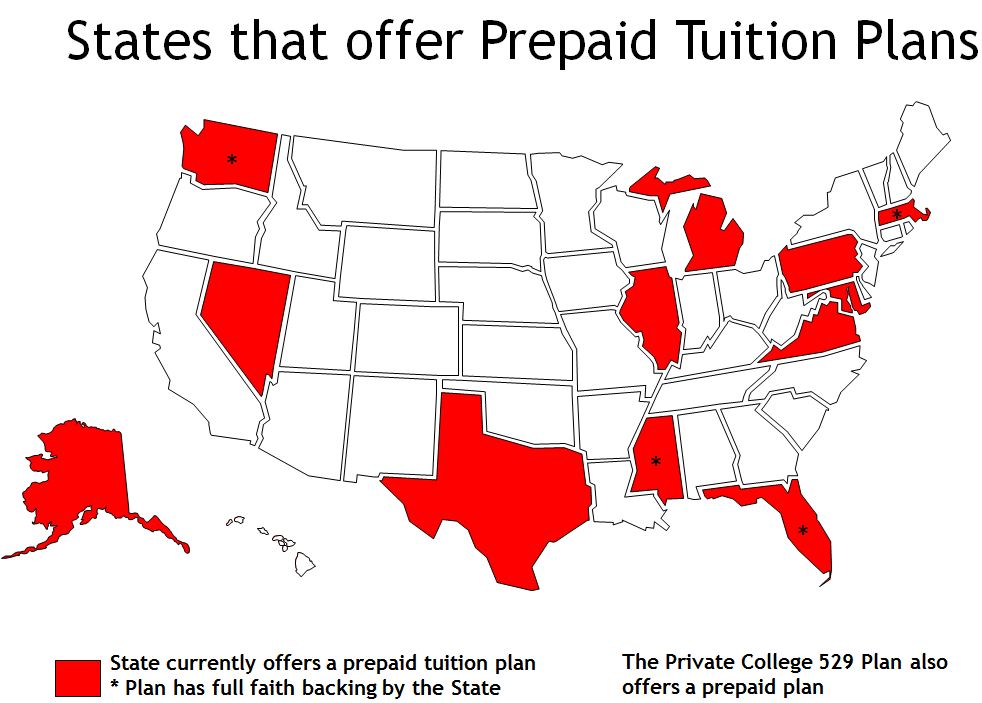

Currently, 12 states and a consortium of private colleges offer a Prepaid Tuition Plan option. See chart below for details.

Both 529 Prepaid Tuition Plans & 529 College Savings Plans enjoy the same tax benefits:

Contributions and earnings in a 529 plan grow free of federal income tax. Withdrawals are tax-free when used to pay for qualified higher education expenses at any eligible college, university, community college or accredited technical training school in the United States or abroad. Many plans also have State tax deductions or credits for contributions or payments to the plan.

If you live in a state that offers a Prepaid Tuition plan, here are a few tips.

Don’t assume that you can only use a Prepaid Tuition Plan at your state’s schools. Plans vary considerably, but most allow you to use the money in your account to attend private, out-of-state schools, and some schools abroad as well.

Your financial adviser may not understand your state’s prepaid plan. Many do, but often financial advisers do not have current or accurate information on the plan that’s available to you. Prepaid plans are only sold directly to investors, with no commission offered to financial advisors.

Ask questions. Go to your state’s website or call the toll-free number and ask what the Prepaid Tuition Plan in your state offers and how it works. Ask about the “payout value” and what promise or guarantee is offered by your state.

Ask about the Plan’s refund policy

Find out the dates of the enrollment period. Note that the cost of participation generally increases each year.

When it comes to investing in a Prepaid Tuition Plan, it is certainly not “one size fits all.” Each prepaid plan has a unique structure and offering and can be a great way to save for college and diversify your portfolio.

Next week’s blog will focus more closely on the unique features that Prepaid Tuition Plans offer. If your state offers a Prepaid Tuition Plan, make sure you check it out to see if it fits your needs. Go to www.CollegeSavings.org to find out what options your state offers.

About the Author:

Betty Lochner is director of Washington’s Guaranteed Education Tuition (GET) program. Under her leadership, the GET program has grown from 7,900 to over 145,000 accounts, with a fund valued at over $2 billion. Washington is unique in that their only 529 plan offered is a prepaid tuition plan. Lochner currently serves as Vice Chair of the College Savings Plans Network (CSPN) and the Chair of the CSPN National Communications Committee.