By Jim DiUlio, CSPN Chair & Administrator of Wisconsin’s 529 College Saving Program

October 8, 2019

Twice a year, the College Savings Plans Network (CSPN) takes a nationwide snapshot of the current accounts and assets in 529 savings plans throughout the U.S. This is useful information to share with the financial media, as well as for state programs and their corporate partners. The totals keep growing as the number of new accounts has increased faster than those that have been spent down for school expenses.

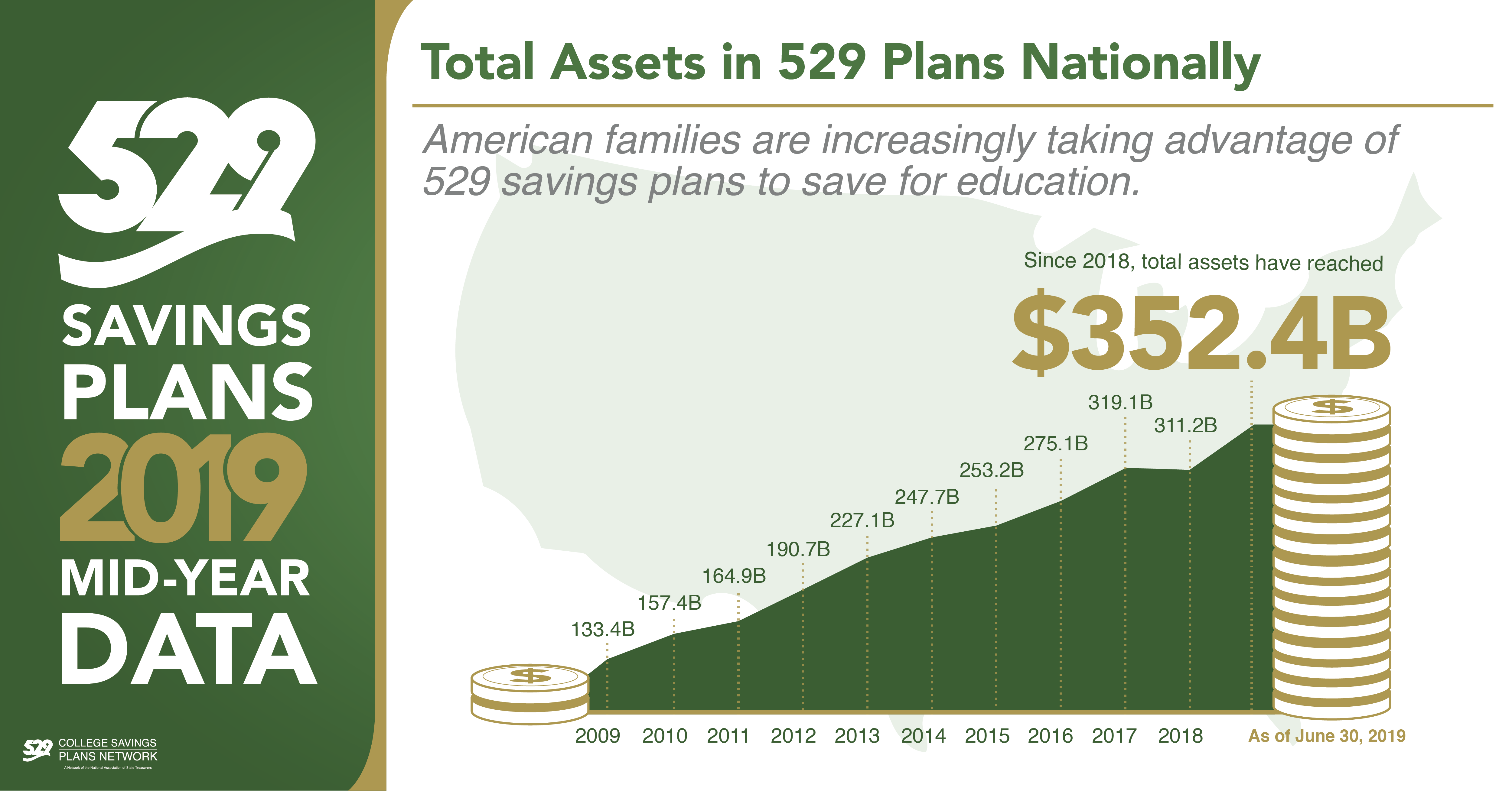

As of June 30, 2019, there are 14 million accounts nationwide, holding $352.4 billion in trust for future education expenses, another record milestone. The total includes both direct-sold and advisor-sold savings plans, along with prepaid and tuition unit contracts, all covered under the 529 umbrella.

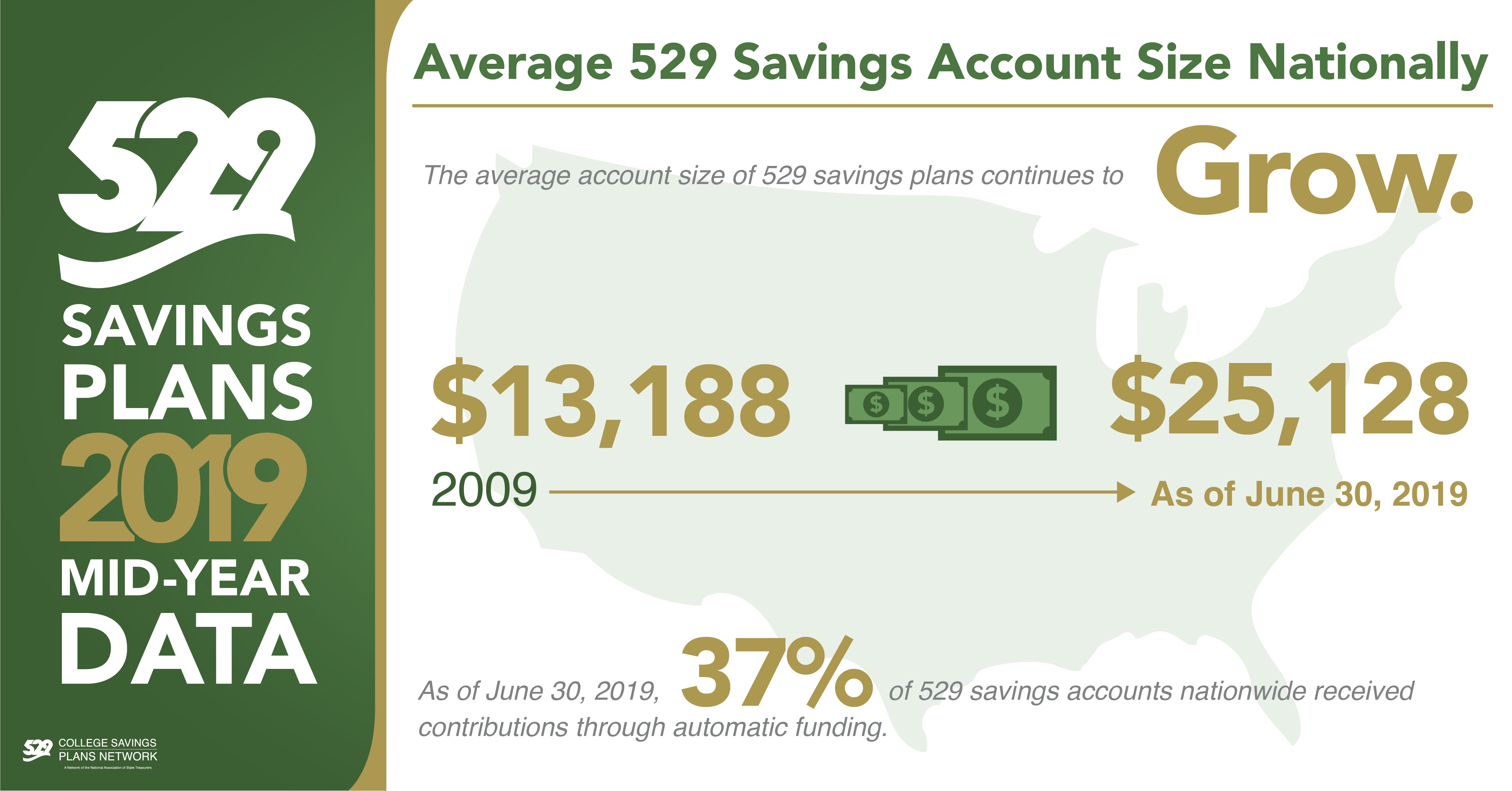

Assets are up 13.2% since the first of the year; the growth comes from a combination of investment performance, new accounts, and increased contributions. The average account size is $25,128.

No matter if you are new to saving for education, or have been at it for years, it’s good to review some fundamental ideas from the investment experts.

No matter if you are new to saving for education, or have been at it for years, it’s good to review some fundamental ideas from the investment experts.

- Periodic savings, as a transfer from a checking or credit union account, or through payroll contributions (an option becoming available at many 529 plans) continue to be popular. In our recent report, 5 million accounts or 37% of the total, are receiving automatic contributions. In addition to convenience, it also encourages a regular habit of savings.

- Asset allocation among investment classes is a way the pros moderate variability of markets and interest rates. Rather than concentrating in just one area—U.S. corporate bonds or only midsize companies—combining multiple funds together in one portfolio can smooth out the bumps of the market. These multiple-fund options in most 529s have names such as moderately aggressive risk or conservative risk, and are reviewed every year or two to maintain the stated investment objectives. While missing an occasional home run, steady is the game here.

- Dedicated tracks that annually change the mix of underlying investments are also popular. Whether based on the child’s current age or the expected year of school enrollment, the experts periodically adjust the underlying investments. An account for a 4-year-old can take some risk, but during the high school years, a conservative path makes better sense. Find links to all the 529 plans and their investment options here.

- Another good idea from the pros is to do a self-review every year. Has your family situation changed? Are your education goals now different? Can you afford to save a bit more? Is the level of risk you take with your investments appropriate? Have your received an unexpected windfall? Your 529 plan website has calculators and information to help you.

- And, although not an investment strategy, 529 plans make it easy and secure for friends and family to also contribute to a student’s future education, online or with gift cards. Every little bit helps!

Just ten years ago, 529 plans held $133 billion in about 10 million accounts nationwide, and the average account size was only half of what it is today. Also at that time, the burden of student loan debt had yet to be realized. So it is gratifying to now see families adding money to their accounts in greater amounts, increasing automatic contributions, receiving gift money from relatives, and being smarter about their investment decisions. As I travel around my state, I enjoy hearing stories from parents of how their increased savings made a difference years later.

While mid-2019 marks another record amount in 529 plan savings, be mindful that the increase is due in part to the growing commitment to higher education families are making. To all of you currently saving in 529 plans, continued good luck to you and your students. And we extend a welcome to those joining the community.

About the Author

Jim DiUlio serves this year as Chair of the CSPN Executive Board. He is the administrator of Wisconsin’s 529 College Saving Program, holding $5.5 billion in trust for 335,000 accounts in its direct-sold Edvest plan and Tomorrow’s Scholar plan, available through financial advisors and fee-only planners.